Blog

Insurer Priorities Focus on Growth Strategies and Stability

It is satisfying when you notice an improvement in your experience of something — when things begin to work the way you like them to. It’s especially rewarding when technology improves the experience so much that it becomes the new standard. A great example of this is how airlines are trying to use technology to overcome jet lag.

In 2005, when the idea of electronically-dimmable aircraft windows was introduced, pundits scoffed at it because they thought it was gimmicky, replacing the plastic slide visor with an expensive gadget. Yet, now the gadget is employed to reduce the shock of long flights on the body by limiting daylight exposure in ways that it will reset the body clock. This is just one of many technologies that can reduce jet lag, including an up-and-coming technology — interior lighting that mimics sunrises and sunsets.

Newer aircraft can also substantially reduce “cabin altitude,” adjusting the pressure to more closely match normal body pressure. Lower cabin altitude means that the body can take in more oxygen. It allows the aircraft to have greater humidity, so you’re less likely to feel like you’ve been walking in the desert. It can also pull in fresh air from the outside. More oxygen, more humidity and fresh air all contribute to improving the flying experience and reducing jet lag. Advanced sensors help aircraft to react to turbulence to smooth out the ride and new aerodynamics use cold air to reduce engine noise. Airlines may still have leg room issues and they may not be the most comfortable sleeping environment, but these technologies help airlines differentiate and grow their business by creating an improved customer experience and value in a highly-competitive industry.

In insurance, we are also the keepers of vital customer experience, including both policyholders and our own employees who need better experiences. Insurance growth strategies can take pages from the playbooks of many different industries that are aiming for growth in the midst of a competitive, complicated and fast changing market.

How can technology foster growth?

Majesco surveyed insurance executives and examined five primary aspects of the insurance enterprise that hold the crucial drivers of insurance growth and profit:

- resource allocation

- business models

- products

- channels

- technology

We looked at what are insurers priorities and how the priorities work for customers, for agents and for employees? Should insurance companies consider shifting investments to reflect a changing set of needs and to improve company operations and growth? Do insurer activities align to their priorities and if not, what does that mean to preparedness for the modern age of insurance? For a complete review, be sure to read the Majesco thought-leadership report, Strategic Priorities 2025: A Modern Era of Insurance Comes Into Focus.

Are Insurer Priorities Aligned to Growth Strategies?

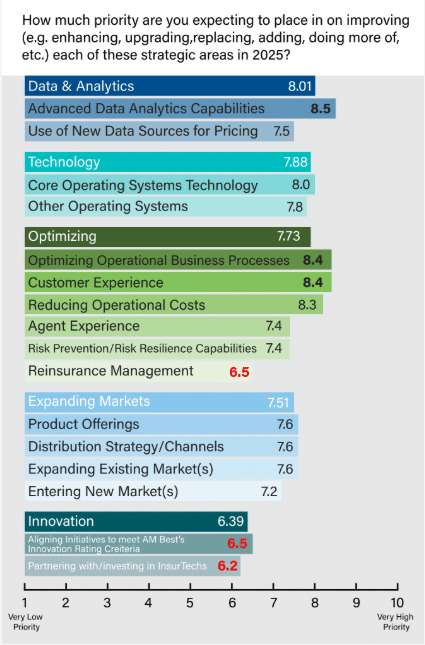

Insurers’ strategic priorities reflect a strong focus on establishing a new technology foundation and optimizing operations to drive growth and profitability as reflected in Figure 1. The combination of core and data and analytics are crucial to a new technology foundation built on a new architecture that is a paradigm shift and groundbreaking leap in software design, fueled by the pillars of modern innovation: cloud-native, API-first, microservices and containerization, headless, and embedded analytics. It is embedded analytics, rather than bolt-on analytics, which will enable insurers to transcend traditional limitations and unlock transformative and optimization potential with embedded intelligence.

Figure 1: Insurers’ strategic priorities for 2025

The new technology foundation improves experiences inside and outside of the organization. On the inside, it provides the ability to produce and communicate actionable insights and optimize business workflows and processes that drive increased productivity and decreased expense ratios. On the outside, it improves customer experiences and empowers leaders to remain competitive and outwardly customer focused.

Data and analytics capabilities are higher in 2025 than in 2024 by 8.6%, reflecting the intense focus on AI, GenAI and Agentic AI in the industry. Close behind is expanding markets with a 17% YoY increase in priority for entering new markets.

Together, these priorities reflect the need to meet growing risks and the shifting market or buyer landscape with rapid advances in data and analytics and next-gen core to deliver the products, customer experiences and reach the channels and markets necessary for growth in a modern era of insurance.

Growth Drivers

Reimaging insurance starts with reshaping a new business model and technology foundation to achieve real optimization, business results, and innovation, to drive growth that is aligned to the future not the past. It requires the right investment and allocation of resources in key areas, including business model, products, channels, and technology.

Resource Allocation

The Majesco survey indicates an upswing in companies reallocating resources to change how they do business in the last year and are also planning to do so in the next three years. They recognize that the pace of change requires a shift in investments to compete.

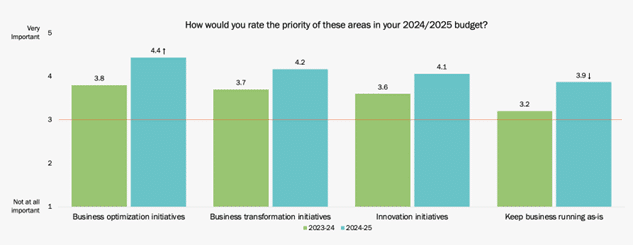

This is reflected in the survey results, where 69% expect their 2025 IT budget to increase – with large increases across all four areas – optimization, transformation, innovation and keeping the business running, as seen in in Figure 2. More importantly, the first three have a higher level of investment than keeping the business running … the first time this has occurred in our research.

Figure 2: Insurers’ budget priorities

Business Models

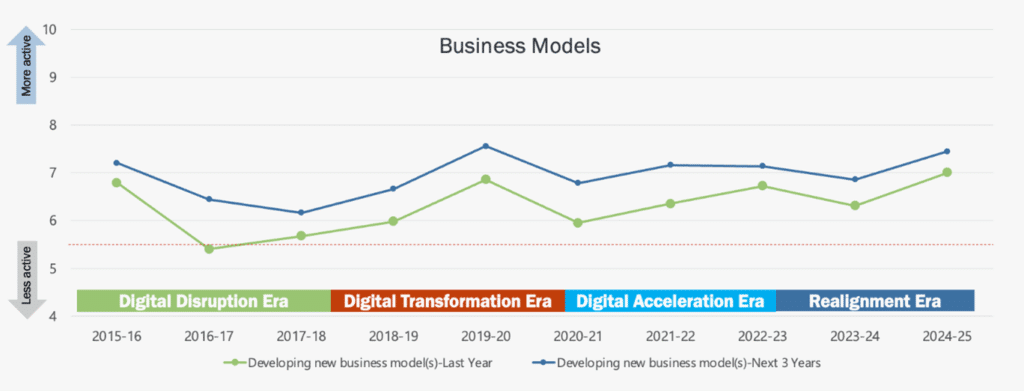

Over the last ten years, developing business models peaked in 2019-20, the middle of the Digital Transformation Era, just prior to the disruption caused by COVID that triggered a downturn. As seen in Figure 3, there is a resurgence in focusing on business models to remain relevant and growing in a modern era of insurance. New risks, customer demographics, and demand for products that are relevant in today’s world are making technology-led business model transformation a method for remaining relevant and growing in a rapidly changing environment.

Figure 3: Insurers’ prior-year and planned strategic activities in developing new business models

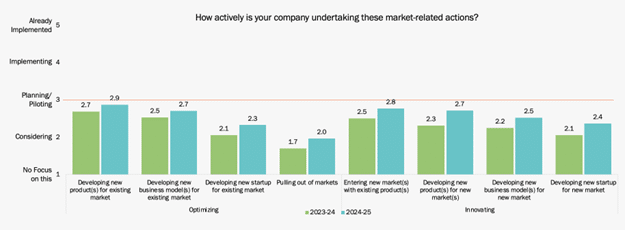

The uptick in business model focus is driven by key areas of increased activity as seen in Figure 4, including developing new business models for existing and new markets and developing a new startup for existing and new markets, all nearly reaching the Planning/Piloting stage.

Figure 4: Insurers’ level of activity in market-related actions

Given the volatility of risk in some markets, pulling out of markets increased — a method some insurers using to stabilize financials. While this is not as high as the focus on business models, it is reflective of the risk environment facing many insurers and not expected to change in 2025.

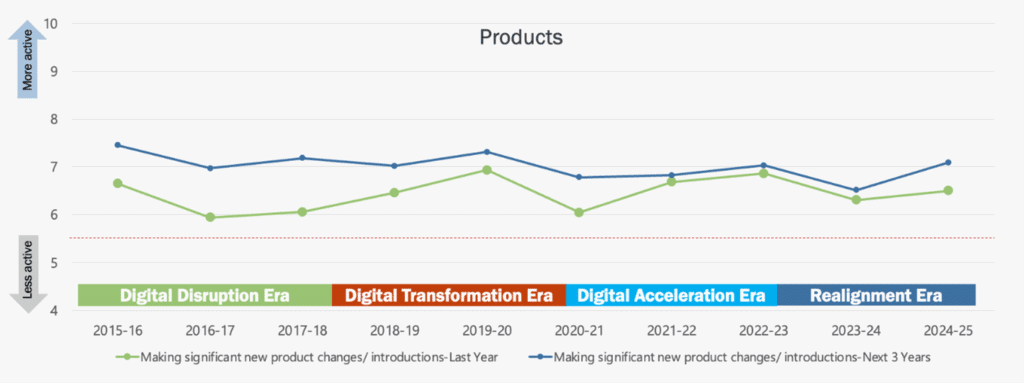

Products

Once again, we see an uptick in focusing on new products or changes to existing products last year, but even more so over the next 3 years as shown in Figure 5. Given the market shifts, this is encouraging and not surprising.

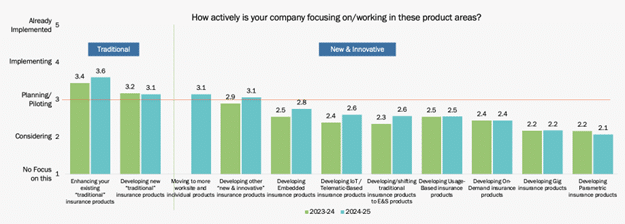

While insurers are still focused on traditional products, their higher year-over-year emphasis on new and innovative products, including worksite, embedded, IoT/telematics-based, and E&S products, reflects their heightened awareness of new risks, shifting market conditions, and customer needs that are driving the development of new products that align to these shifts that will drive growth (see Figure 6).

Figure 5: Insurers’ prior-year and planned strategic activities in developing new products

With dramatic increases in insurance prices for consumers and businesses, J.D. Power anticipates 2025 will see increased adoption of telematics-based pricing and usage-based insurance (UBI) policies that track driving patterns to offer discounts. Currently, according to J.D. Power, only 17% of drivers purchase UBI policies. This plateau is partly due to insurers reducing UBI offerings in 2024 to focus on profitability through rate hikes, with only 15 percent of shoppers being offered UBI programs, down from 22 percent in 2023.[i]

With the increasing frequency and severity of weather events and wildfires, parametric insurance is becoming an important product to help bridge some of the protection gap. It provides immediate financial assistance to victims of these severe events.[ii] Automatic payouts are triggered when certain thresholds are met, such as wind speed or water depth. They can assist with immediate needs for temporary shelter, food, or other necessities in the aftermath of the trigger event, while the full claim is processed through the customer’s traditional insurance coverage. Given the increasing need for this type of product, insurers should move it out of the “considering” phase.

From a L&AH perspective, demographic changes and employees moving more regularly between jobs demands innovation in products to meet changing needs, resulting in a shift to individual life, annuity and supplemental and worksite products. In addition, insurers who offer group and voluntary benefits are looking at new products that are affordable given that rising medical and healthcare costs are challenging enrollment of other lines of business beyond medical, vision and dental.

Figure 6: Insurers’ level of activity in traditional and new product areas

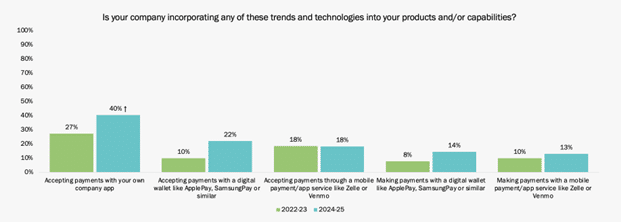

Insurers continue to make progress in digital payment capabilities as shown in Figure 7. Two years ago, only 27% of insurers accepted payments with a dedicated company app. That has now jumped to 40%. While accepting payments via digital wallets like ApplePay or Samsung Pay is at half that level, they also doubled in usage over two years.

Figure 7: Insurers’ use of digital payment technologies

Making payments to customers for claims via a digital wallet or payment app, while lower than accepting payments, continues to rise. This will continue to grow, given the challenges of getting money to customers when their homes are gone from cat events.

Channels

In today’s interconnected world, insurance must play across a wide spectrum of distribution options, expanding channels and partners to reach customers when, where, and from whom they want to buy insurance. These options form a distribution ecosystem that expands reach.

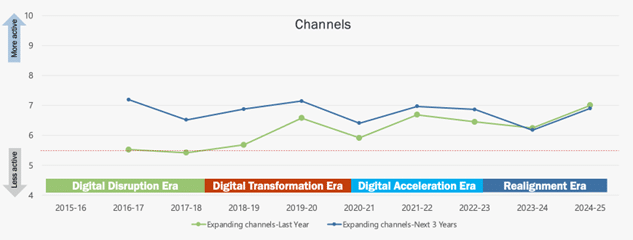

Channel trends took a significant upswing as compared to the previous four years as shown in Figure 8, following the same path as the other strategic activity trends and highlighting the need for distribution options.

The gap between the previous year and next three years has been converging over the last 8 years and is nearly in alignment this year. This reflects the heavy focus the last ten years of InsurTech on distribution with the industry’s continued expansion beyond independent agents to other channel options and the progress made.

Figure 8: Insurers’ prior-year and planned strategic activities in expanding distribution channels

In addition, during this time the demise of the agent channel never came to fruition … rather it gained strength and value, particularly given the market and risk challenges. While it remains dominant, new channels, such as marketplaces and embedded insurance, are gaining a lot of attention and traction.

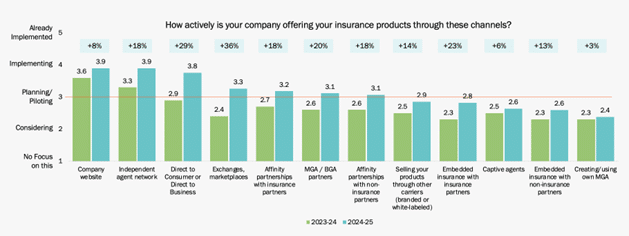

This is reflected in the increases across every channel option in the survey, as highlighted in Figure 9. The most impressive increases came in exchanges and marketplaces (+36%), direct to consumer/direct to business (+29%), embedded insurance with insurance partners (23%), MGA/BGA partners (+20%), and affinity partnerships with insurance and non-insurance partners (18%).

Figure 9: Insurers’ level of activity in developing/expanding channels

Insurers looking to compete will find it challenging to do it alone, particularly given that the competition is rapidly expanding their channel ecosystem to offer more reach and avenues for growth.

While expansion is important, ensuring “ease of doing business” with any of the channels is equally important from a growth and retention perspective.

Insurers face looming issues of an aging workforce, rising customer expectations and changing needs, and the need for next-gen technology, including agent portals. Agents have high expectations for how insurers will support them today and have even higher expectations for how insurers will support them tomorrow.

Technology

The cost and impact of legacy debt is now catching up and pulling organizations down – strategically and operationally. With increasing retirements and loss of institutional knowledge and skills, coupled with a new generation of employees who will not work with legacy technology, legacy debt is becoming a significant operational risk. Even worse, these patchwork legacy solutions struggle to leverage the data they hold to provide meaningful, actionable insight or ingest new data sources to improve decision-making.

Competing in today’s marketplace requires speed to market for new products, channels, and experiences; a decrease in operational costs and total cost of ownership of technology; continuous innovation; and seamless and quick technology upgrades to keep the business at the leading edge.

Industry leaders are changing the rules of insurance by leveraging the powerful next-generation intelligent solutions to launch a new business operating model with new products and then converting business that is part of the future to enable speed and scale. Across each of these technology areas, there is a significant uptick in focus, a glimmer of optimism that legacy is being dealt with.

Majesco leads the way in helping insurers to transform their legacy systems and business models. We have designed technology solutions to address every aspect of the experience — from the back office through to the end customer. Majesco’s intelligent core systems utilize AI, GenAI and Agentic AI, improving workflow while automating communications, tasks, insight gathering and insight delivery — driving significant operational optimization and reduction in expense ratios. Our CoreConnect technologies are simplifying complex processes for MGAs using cloud-native next-gen platforms. In every way, Majesco solutions are helping companies to course correct — driving them toward long-term growth, stability and resiliency. For additional perspective on MGA technology opportunities, be sure to register for Majesco’s upcoming webinar, Unlocking MGA Growth Momentum: New Insights and Priorities to Compete.

[i] Sclafane, Susanne, “2025 Underwriting Profit and ‘Shop-a-Palooza’ Predicted for Auto Insurance,” Carrier Management, December 31, 2024, https://www.carriermanagement.com/features/2024/12/31/270001.htm?utm_content=shop-a-palooza-what-to-expect-for-personal-auto-insurance

[ii] Weiss, Suzanne, “Parametric Insurance Can Offer Prompt Payout When Disaster Strikes,” National Conference of State Legislatures, January 15, 2025, https://www.ncsl.org/state-legislatures-news/details/parametric-insurance-can-offer-prompt-payout-when-disaster-strikes